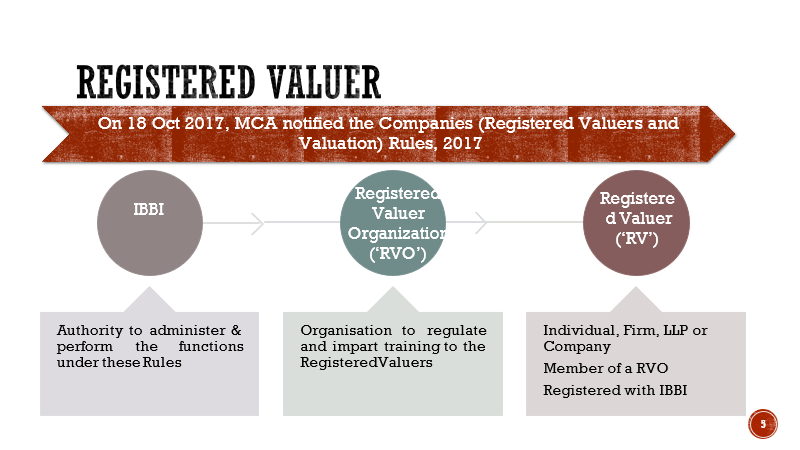

REGISTERED VALUER

Section 247 of the Companies Act, 2013 (‘Act’) provides:

- Valuation of property, stocks, shares, debentures, securities, goodwill or other assets / liabilities / net worth of a company under the Act

- To be done by a Registered Valuer (RV)

- Appointed by Audit Committee or in its absence the Board of Directors of that company

Further, as per Section 247(2) of the Act, RV shall

- make an impartial, true and fair valuation of assets;

- exercise due diligence while performing the functions as valuer;

- make the valuation in accordance with such rules as may be prescribed; and

- not undertake valuation of any assets in which he has a direct or indirect interest or becomes so interested at any time during a period of three years prior to his appointment as valuer or three years after the valuation of assets was conducted by him.

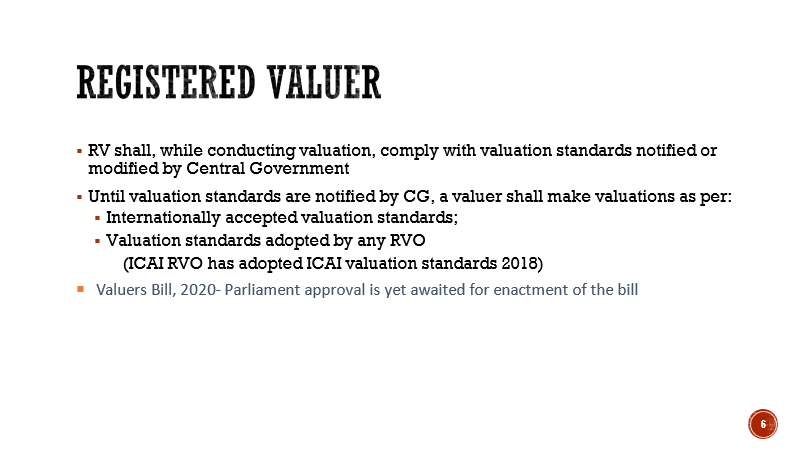

- RV shall, while conducting valuation, comply with valuation standards notified or modified by Central Government

-

Until valuation standards are notified by CG, a valuer shall make valuations as per:

- Internationally accepted valuation standards;

- Valuation standards adopted by any RVO

- Internationally accepted valuation standards;

- Valuers Bill, 2020 – Parliament approval is yet awaited for enactment of the bill

Our offerings

- Business Valuation

- ESOP accounting- Intrinsic Value and Black Scholes

- ESOP for Taxation

- Acquisition – Domestic & Cross Border

- Merger – Assessment of Swap Ratio

- Fairness Opinion

- Valuation for spinooff/restructuring

- Share Purchase / Investment/Fund Raising

- Good will & Asset Impairment testing (US GAAP/ IFRS/Indian GAAP)

- Foresnsic Valuations including court cases and legal proceedings

- Valuations for Family settlements

- Brand valuation

- Intellectual property valuation

- Asset valuation for purchase price allocation (US GAAP/IFRS)

- Carried Interest valuation

- Derivative Valuation under IFRS